What Does a 500 Credit Score Mean for Borrowers?

14 Min Read

Soft credit checks are a routine part of financial life, giving organizations a way to access limited credit information without affecting your borrowing ability. You may encounter them while checking your own financial report, browsing credit card options online, renting a car, or managing an existing account with a lender. Soft credit pulls are also commonly used during preapproval for certain loan products or mortgage offers.

Unlike hard inquiries, soft checks are largely behind-the-scenes, meaning they won’t appear on reports that lenders see when deciding on new credit. Being aware of their role can help you interpret your credit activity more clearly and avoid unnecessary concern when you notice these inquiries on your report.

Key Takeaways

- A 500 credit score is considered poor. However, borrowers with such a rating may still be approved for certain loans, though with higher costs and tighter rules.

- The most practical tools for rebuilding are secured credit cards, credit-builder loans, or certain subprime loans. Most traditional bank products won’t be available at this stage.

- It’s still possible to improve the score via simple habits. Start by paying on time, keeping balances low, and avoiding new mistakes.

A credit score of 500 usually signals past financial problems or limited borrowing experience. This makes lenders more cautious. While approval isn’t impossible, it can be tough to qualify for unsecured loans or credit cards on favorable terms.

This guide breaks down what this score means, what may cause it, and how lenders and borrowers handle it. You’ll learn how to avoid costly mistakes and focus on solutions that really improve your rating.

What Is a 500 Credit Score?

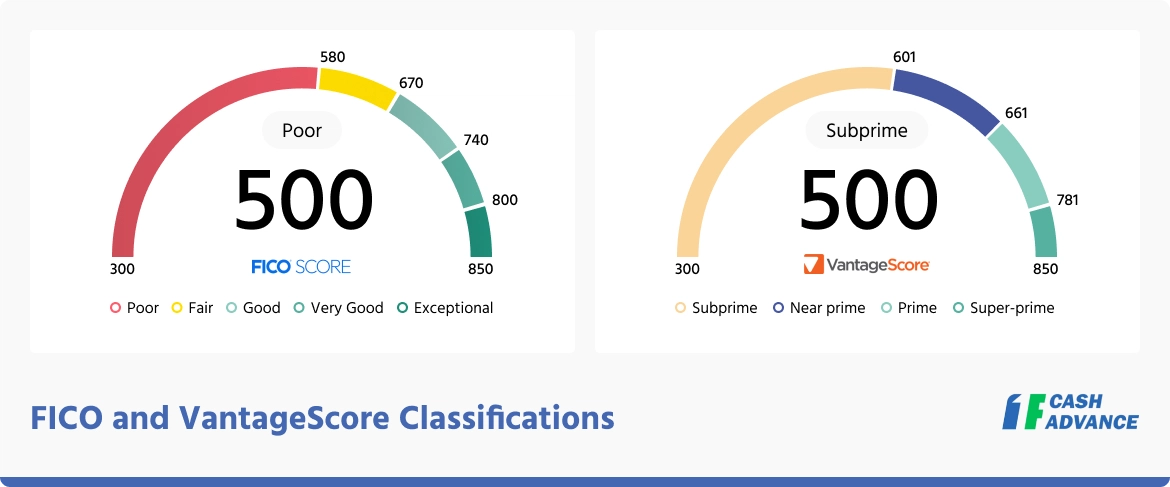

A 500 credit score is a three-digit measure of your credit and financial behavior on the scale from 300 to 850. The average credit score in the United States is currently 715. Data from the Consumer Financial Protection Bureau shows that about 14.2% of U.S. adults have credit scores below 580. Although FICO and VantageScore use different labels, this range signals high credit risk in both scoring systems.

Below are FICO and VantageScore classifications:

A poor credit score is often a signal of a lack of credit history, late payments, defaults, or long-term financial issues. In simple terms, lenders assume that there’s a higher risk that the person with such a score might not be able to repay the loan on time.

Having a credit score of 500 surely limits options and overall access to low-cost loans. Many banks and online lenders will either decline applications right away or offer less favorable terms and higher interest rates.

What Causes a 500 Credit Score?

A credit score this low is typically the result of multiple negative factors building up over time; it’s rarely just one isolated mistake. Let’s explore what actions decrease the rating the most.

Missed or Late Payments

Payment history is the most influential factor in a borrower’s credit score, accounting for 35% of it. Repeated late payments, accounts reaching 60 or 90 days past due, and charge-offs all drag the score down. Even after the balance is paid off, the record of missed payments will remain on a credit report for up to 7 years.

High Credit Utilization

Using a large portion of your available credit card limits may work against you, as it indicates financial strain to lenders. Maxed-out cards or balances close to the limit can reduce your scores, even if you’re still making the minimum payments on time.

Accounts in Collections or Default

Unpaid medical bills, utilities, personal loans, or credit cards sent to collections can push a score into the very poor range. Collections are considered a major indicator of the ability to repay any loan.

Short or Disrupted Credit History

A limited borrowing history, closed long-standing accounts, or long periods without credit activity can also decrease the score. Lenders prefer borrowers with a stable track record, and such gaps make it harder to assess the potential for default.

Frequent Credit Applications

Applying for multiple loans over a short period results in several hard inquiries. While each has a small effect, combined, they can lower an already fragile score even further. It can also signal financial pressure to lenders.

What Can You Get with a Poor Credit Score?

Even though a FICO score of 500 is very low, it doesn’t mean that any loan application will be denied. Still, borrowing in such conditions usually results in higher APRs and less favorable terms.

When you know your options and understand how each of them actually works, you can focus on the ones that make sense and don’t waste time on applications that are unlikely to be approved.

Credit Cards

With a score of 500, access to traditional unsecured credit cards is extremely limited. When approvals do occur, they usually come with low card limits, annual fees, and very high interest rates designed to offset the lender’s risk.

Secured credit cards are far more common and accessible. They require a refundable cash deposit that usually becomes your spending limit. Because the lender’s risk is reduced, approval standards are lower, and responsible use can help rebuild a score over time. Keeping balances low and paying the statement in full each month is recommended to recover your credit rating faster.

To clarify the practical differences for someone with a 500 score, here’s how secured and unsecured cards compare:

| Feature | Secured Credit Card | Unsecured Credit Card |

|---|---|---|

| Approval requirements | Easier to qualify with poor credit | Very limited with a 500 score |

| Upfront deposit | Required (refundable) | Not required |

| Credit limit | Usually equals deposit | Based on creditworthiness |

| Interest rates | High, but manageable if paid monthly | High, often with added fees |

| Fees | Usually lower | Often includes annual fees |

| Credit-building value | Strong if used responsibly | Strong if used responsibly. However, borrowers with 500 scores have limited access to this option |

Personal Loans

Since most banks and credit unions generally require scores of 620 or higher for approval, it’s hard to get approved for a traditional loan with a 500 score. For such situations, there are subprime or alternative lenders with more relaxed requirements. However, they typically apply higher APRs, extra fees for verification or origination, and very tight repayment terms. Such lenders focus on the stability of income and recent payment behavior instead of credit history in general.

Here’s a snapshot of typical personal loan APR ranges by credit tier:

| Credit Score Range | Average APR |

|---|---|

| 300–629 | 21.65% |

| 630–689 | 17.93% |

| 690–719 | 14.48% |

| 720–850 | 11.81% |

Payday Loans

This type of alternative borrowing usually targets people with very poor credit because lenders mainly focus on income. This makes payday loans easy to get. Approval is often quick, and credit checks are usually soft and do not affect your FICO rating. Repayment terms typically range from 14 to 31 days. The amounts available differ by state and the borrower’s profile.

Due to their high cost (APRs often exceed 400%) and short repayment periods, payday loans may be difficult to repay on time, leading to repeated borrowing and mounting fees.

Installment Loans

These loans are advertised as a more affordable alternative to payday loans, because they allow borrowers to repay over multiple monthly payments instead of a single lump sum. Even though payments seem more manageable, APRs and other fees remain very high for applicants, often exceeding 200%.

Not all installment loans have the same eligibility criteria and terms, as each company operates differently depending on numerous variables. What matters most is whether the lender reports on-time payments to credit agencies, helping you rebuild your financial profile.

Auto Loans

With the tighter conditions in place, borrowers may be approved for auto financing even with a 500 credit score. To minimize the risk of default, lenders usually require a down payment and limit loan amounts and the age of the car. Apart from that, interest rates tend to be substantially steeper than those you could get with good credit. This means you pay much more than the original price.

In some cases, borrowers may be approved only through specialized subprime auto lenders. Make sure to weigh carefully if the monthly installments fit comfortably within your budget, and the current need for a vehicle is actually worth the effort and final amount paid.

Here’s how auto loan interest rates usually vary by credit score:

| Credit Score Range | New Car APR | Used Car APR |

|---|---|---|

| 300–500 | 15.81% | 21.58% |

| 501–600 | 13.22% | 18.99% |

| 601–660 | 9.83% | 13.74% |

| 661–780 | 6.70% | 9.06% |

| 781–850 | 5.18% | 6.82% |

Mortgages

With a FICO score below 580, qualifying for a home loan is extremely difficult. Most conventional lenders require higher scores, but government-backed options, such as FHA loans, are available at this level.

To get approved, you need to pay a higher down payment of at least 10% of the house price, show steady income, and have a favorable debt-to-income ratio, too. Given the complexity and severe requirements, the best decision may be to take some time to improve a credit score before a mortgage application.

Rent

You can rent an apartment with a low credit score, but it will require extra effort. Most landlords adjust to financial reality and become less picky. They don’t base their decisions solely on the rating and consider other factors, including income, employment history, and even references from prior rentals.

Still, property managers may ask for a higher security deposit, proof of steady income, or even a co-signer to mitigate the risk of missed payments. Learn more about emergency options for rent payments.

How to Improve a 500 Credit Score

There are no quick fixes or one-time actions when it comes to rebuilding a credit profile. It’s a very slow process based on steady, mindful steps. While progress may feel too sluggish at first, the right approach lays a foundation that allows your score to recover steadily.

Create a Strategy to Manage Your Current Debt

The number one thing is to gain control over existing debt and the overall financial situation. Review all the open accounts, together with balances, interest rates, and due dates. Accounts that are past due or in collections must be addressed first, as ongoing missed payments keep damaging the profile.

Bringing accounts up to date helps stop further score decline, even if you can only make partial or negotiated payments. As late payments are especially damaging to a credit score, you can reduce this risk by setting up automatic payments in the online banking app for at least the minimum due.

Review Your Credit Reports to Spot Inaccuracies

Confusion in financial reports happens more often than many people think. Even small errors can have a huge impact on records. By regularly checking reports from all credit bureaus, you can identify incorrect balances or accounts that don’t belong to you. You can do this for free once a year at AnnualCreditReport.com.

If you find errors, file a dispute to remove inaccurate data or correct it. Even though not all revisions result in a score increase, removing incorrect information guarantees your score reflects your actual credit background, not just someone’s reporting mistakes.

Use a Secured Credit Card to Rebuild Payment History

A secured credit card is often one of the most effective tools for rebuilding your score from a very low starting point. Because the card is backed by a cash deposit, approval standards are lower, and the risk to the lender is reduced.

What matters most is how you actually use this card. Using only a small portion of the credit limit and paying it off in full each month helps build a positive payment history. In the long run, it offsets past negative behavior and shows lenders that your habits have changed.

Open a Credit Builder Loan

Credit builder loans are designed specifically for people who are working to improve their standing. Instead of receiving funds upfront, payments are made toward a locked savings account, which is released once the loan is paid off. Each on-time payment is reported to the major credit bureaus, helping establish a record of reliability.

These loans are most effective when payments are made consistently and on time. Because the loan is structured around saving, it builds credit history without increasing overall debt, unlike traditional loans.

Report Rent or Monthly Bills When Possible

For borrowers trying to rebuild their financial profile, the most essential thing is to add new, positive data to their record. Services such as Experian Boost, RentReporters, and LevelCredit allow reporting different timely payments to credit bureaus (rent, utilities, or phone bills). In such a way, you may turn ongoing monthly obligations into chances to enhance your credit.

This activity doesn’t carry as much weight as traditional borrowing products, but it still improves the broader picture, indicating your financial responsibility. In combination with on-time loan or credit card payments, it contributes to the overall progress and adds more positive marks to the track record.

How Long Does It Take to Improve a Credit Score?

A borrower’s profile enhancement won’t happen overnight, and any marketing campaign promising instant results should be treated cautiously. Credit scores change based on reported behavior, and those financial patterns take time to establish.

In most cases, small improvements may appear within the first 3 to 6 months if there are no missed payments and all errors on credit reports are corrected. You’ll often see early gains after catching up on overdue accounts, reducing card balances, or successfully disputing inaccurate information, if any.

More serious progress normally takes 6 to 12 months of steady, on-time payments and responsible credit use. During this period, lenders begin to see a pattern of stability rather than isolated positive actions. Moving from very poor credit into the fair range usually requires this level of sustained effort.

Reaching a good score from 500 often takes 1 to 2 years or longer, depending on how severe the original issues were. Collections, charge-offs, and defaults do not disappear quickly, but their impact fades as newer, positive information is added to your credit report. Sticking to the pre-arranged plan matters more than anything else. A single late payment can wipe out months of hard work and progress, while consistent behavior accumulates and moves your score up.

Conclusion

A 500 credit score can feel discouraging, but it doesn’t have to define your financial future. While borrowing at this level is more expensive and limited, access to credit still exists, and improvement is absolutely possible.

The most important thing is to avoid decisions that create short-term relief at the cost of long-term damage. Late payments, repeated applications, and defaults can hold your score back and keep it in the subprime range. You can gradually rebuild trust with lenders, even conventional ones, when you borrow mindfully, ensure accurate credit reporting, and develop consistent repayment habits.

FAQ

Is a 500 credit score bad?

A credit score of 500 is considered very poor. It is well below the average rates in the United States and heavily limits borrowers’ access to affordable loans and credit cards. Still, it may be rebuilt with consistent effort and improved financial habits.

Can you get a loan with a 500 credit score?

With such a low score, options are limited, but you may be approved by subprime lenders. Please note that such loans come with higher interest rates, extra fees, or less favorable repayment terms to offset the risk of default.

What is the fastest way to improve a credit score?

The first and most important step in rebuilding your score is to stop missing payments as soon as possible. The next steps are to verify your report for any mistakes and try to lower your credit card balances. They won’t enhance your profile in the blink of an eye, but they will start moving things in the right direction and prevent further damage.

Will applying for a loan hurt my credit score?

Since most loan applications require a hard credit check, it can decrease your score by several points, which may seem minor. However, several applications in a short period can have a larger impact, particularly when your score is already low.

How much can I borrow?

Typically, there are limited amounts for applicants with low FICO scores. The exact amount, terms, and repayment schedule vary by lender and state regulations. Plus, add income, current debt, and any possible collateral requirements here.

What can I get with a 500 credit score?

With a FICO score in this range, borrowers are most likely to qualify for secured credit cards, certain subprime personal or auto loans, FHA mortgages, and a few short-term financing products. These options usually come with higher interest rates, lower limits, and tighter terms, so it’s important to weigh the costs carefully and ensure they fit your budget.

Explore short-term loan options designed for real people, not perfect credit histories!Apply Now