1F Cash Advance Expert Guides and Articles

We're excited to announce that the 1F Cash Advance Team of financial writers has been working hard to bring you the best lending information possible.

Our 10-year expertise in the lending industry is a valuable asset in helping you understand how different loans work and what options are available to you.

Our goal is to arm you with the knowledge and confidence needed to make informed decisions about your finances.

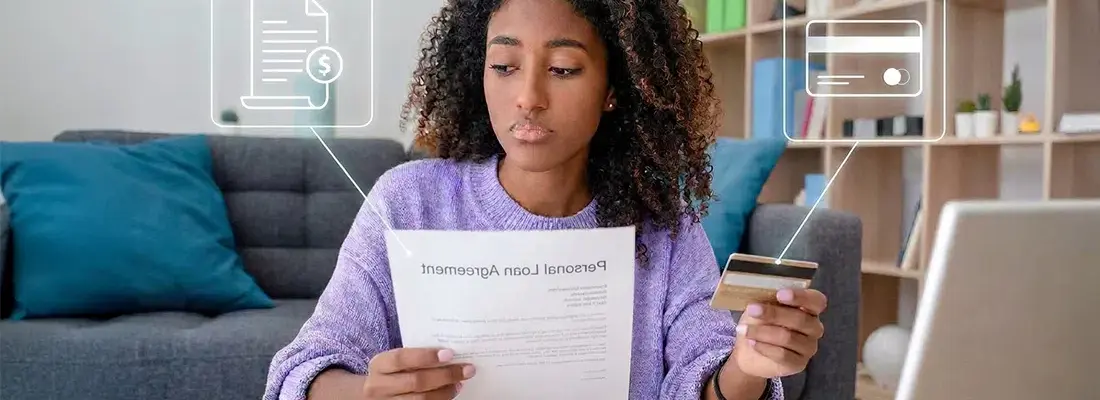

Personal Loans vs. Credit Cards: How They Differ

Both personal loans and credit cards can provide you with money for personal needs. However, they don’t work the same and fit different life situations. Personal loans provide you with a fixed amount upfront and require you to gradually repay it over time with interest in equal monthly installments. Credit cards give you ongoing access to funds up to a specific limit and offer more repayment flexibility. Here’s a closer look at both options to help you better understand which one will work for you.

Top-rated

Top-rated

Best Options for Short-Term Loans in 2026

Short-term loans can cover an emergency expense fast, but in 2026 the best choice depends on your state rules, the total cost, and how quickly you can repay. This guide explains the main short-term options, shows key red flags to avoid, and tells how 1F Cash Advance can help you make the safest choice.

Top-rated

Top-rated

10 Fast Ways to Cover Emergency Expenses

Most Americans would struggle to cover a $1,000 emergency. Not every emergency requires a loan, though. This guide explains how to tell if something is a real emergency and covers 10 ways to handle emergency expenses.

Top-rated

Top-rated

Emergency Cash for Single Mothers

Single moms facing financial emergencies can benefit from grants and loans. Get help with housing, pay bills, and receive medical aid and child care services.

What Are Your Real Loan Options with a 400 Credit Score?

While a 400 credit score is considered poor on both FICO and VantageScore scales, you can access several types of loans with a score that low. However, not all lenders will approve you, and you are likely to get higher interest rates and fees, shorter repayment terms, and lower loan limits. We explore loan products that people with poor credit can potentially get and discuss their rates and terms so you know what to expect.

Line of Credit vs. Loan: What’s the Difference?

Both loans and lines of credit can be used to cover personal expenses or reach major life goals. However, they work differently and can outperform each other depending on the situation. While personal loans give you a lump sum of money with a fixed rate and repayment over a specific period, lines of credit provide you with on-demand access to funds up to a set limit, with interest charged only on the amount you actually use. The article breaks down how these products work and when they may be a good fit.

Small Business Loans: Types, Rates, and How to Qualify in 2026

Running a small business in 2026 brings financial pressure, from uneven revenue to rising costs. When cash flow tightens, loans can help cover expenses. Options like SBA loans, lines of credit, and factoring serve different needs.

What are your loan options with a 600 credit score

A 600 credit score is considered fair on both FICO and Vantage scoring models. Although it poses certain risks to lenders, you can still get different loan types with such a score. Let's find out how lenders treat borrowers with a 600 score, what financial products are available to them, and how to improve your score to access better loan options in the future.

Top 7 Loan Apps for 2026

Unexpected expenses can throw off even a well-planned budget. Loan apps provide quick access to small amounts of money, often without credit checks, but fees and limits differ widely. Some options are cheaper and more predictable than payday loans, while others can quietly increase costs. Choosing the right service and borrowing carefully makes all the difference.

What Does a 500 Credit Score Mean for Borrowers?

A low credit score changes the rules of borrowing. From higher rates to limited approvals, this article explains what everyday financial life looks like with a 500 score and what can realistically improve it.

Things to Know About a Soft Credit Check

Soft credit checks happen more often than most people realize. They’re used to review basic credit details without affecting your score, especially when you explore loan options or manage existing accounts. Knowing how these inquiries work helps you read your credit report clearly and avoid confusion when borrowing short-term.

How Do Loans with Same-Day Funding Work?

Same-day loans can be a great way to access emergency funding when urgent needs arise. However, you need to consider your options carefully. In some cases, such loans come with high APRs, short payback times, and risks of debt cycles. This article explains how emergency same-day loans work, explores available loan types, and provides smart tips on making an informed loan choice.

Top 5 Small Loan Options with No Credit Check in 2026

Short-term loans without credit checks have become a common solution for covering unexpected expenses. This article breaks down how these products work, what they cost, and which options may be better depending on your financial situation in 2026.